Here is what Jeremy Hunt’s Spring Statement will mean for your bank balance

Jeremy Hunt and Rishi Sunak are getting prepped for the Spring Statement on March 15. Here’s everything you need to know about what it could mean for your bank balance

by:

9 Mar 2023

Chancellor Jeremy Hunt is set to announce the Spring Statament on March 15. Image: No 10/ Flickr

Share

The fate of our bank balances (and the future of the country’s finances) is in Jeremy Hunt and Rishi Sunak’s hands as they plan for the Spring Statement 2023.

The Spring Statement, on March 15, will have to take some of these issues into consideration. Ministers have repeatedly claimed they will forge a plan to “tackle the cost of living crisis and rebuild the economy”. But will the Spring Statement make steps to achieve this? And how will it impact our household income?

Experts at the Resolution Foundation have set out their predictions for the budget, warning that while the economy is making progress, people will still feel the pinch over the next two years.

Here’s what you need to know about the predictions for the Spring Statement and what it will mean for you, covering energy bills, taxes, benefits, cost of living payments and more.

Advertising helps fund Big Issue’s mission to end poverty

Advertisement

How much will my household income fall in 2023?

Your bank account is likely to take another hit this year. In real terms, compared to prices, household incomes are set to fall by 2 per cent in 2023, according to the Resolution Foundation. That’s the equivalent of around £700 this year, up to 4 per cent between 2023 and 2024, around £1,100.

This could have an impact on our savings, but the economic jury is still out on which way it will go. The Office for Budget Responsibility so far assumes savings will fall as people dig into their accounts to make up for the rising cost of living, while the Bank of England is actually forecasting a rise in savings. At the moment, the difference between these two forecasts is big (worth nearly £40 billion).

The OBR produces forecasts for the economy and public finances twice a year to coincide with the Autumn and Spring Statements, so we’ll have a clearer idea of where the OBR lands on Wednesday.

What is happening with energy prices?

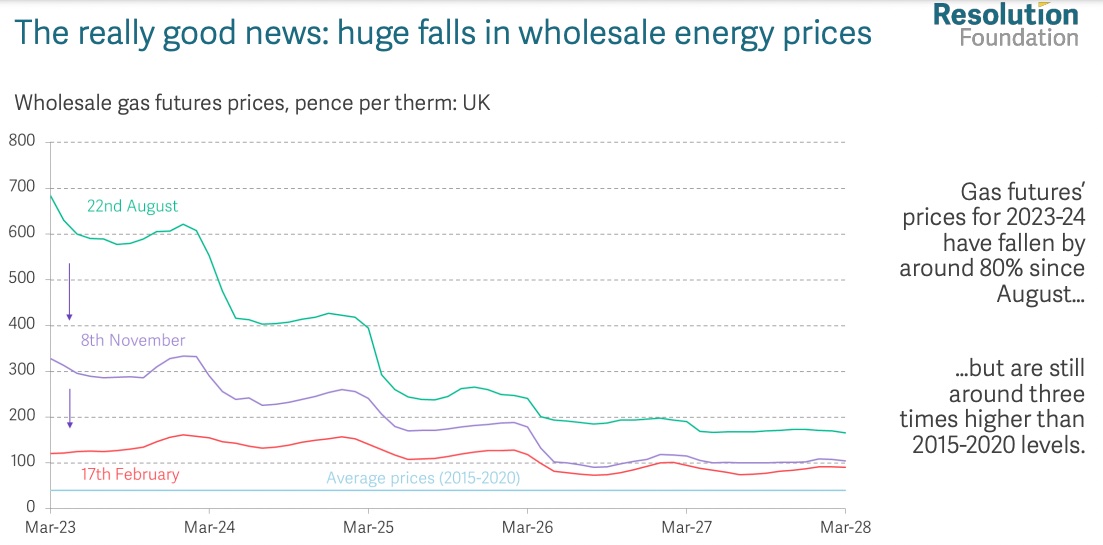

Ready for some rare good news? Wholesale energy prices have fallen hugely since their peak in August. This graph from the Resolution Foundation shows that gas futures’ prices (a national benchmark price) have fallen by around 80 per cent. This is a bigger drop than was expected when the government set out the Autumn Statement.

Prices are still high – in fact, they are around three times higher than the average level between 2015 and 2020.

Will the government delay the increase in the energy price guarantee in the Spring Statement?

It is likely that the government will delaythe increase in energy price guarantee, as reported by the BBC.

Advertising helps fund Big Issue’s mission to end poverty

Hunt said in the Autumn Statement that the guarantee, currently capping household bills at an average of £2,500, was going up to £3,000 in April, but money saving expert Martin Lewis and some of the UK’s leading charities have been calling for the chancellor to scrap this plan.

The drop in wholesale gas and electricity prices has made this possible. Through the guarantee, the government essentially makes up the difference between what households are paying and the cost of buying energy from wholesale markets.

If the Ofgem price cap system still determined how much households pay on energy, typical energy bills would have risen to £3,280 from April. The government’s price guarantee offers some protection from that – and, if reports are accurate, typical bills should remain at around £2,500 a year.

Avoiding a sharp rise in people’s energy bills by maintaining the energy price guarantee at £2,500 for three months would cost around £3 billion, according to the Resolution Foundation.

The government is yet to confirm or deny these plans and has reportedly asked energy firms to prepare for both scenarios, leaving anxious households waiting until the Spring Statement to see if their energy bills will go up in April.

So, what does this mean for our energy bills?

If the government keeps the energy price guarantee in place, a typical household’s energy bills will remain at around £2,500 a year. But the chancellor has confirmed that the energy rebate is set to end this month. This was a £400 discount on energy bills over the winter months and the end to that might come as a jolt to household incomes (even if heating bills are less expensive in the summer months).

Advertising helps fund Big Issue’s mission to end poverty

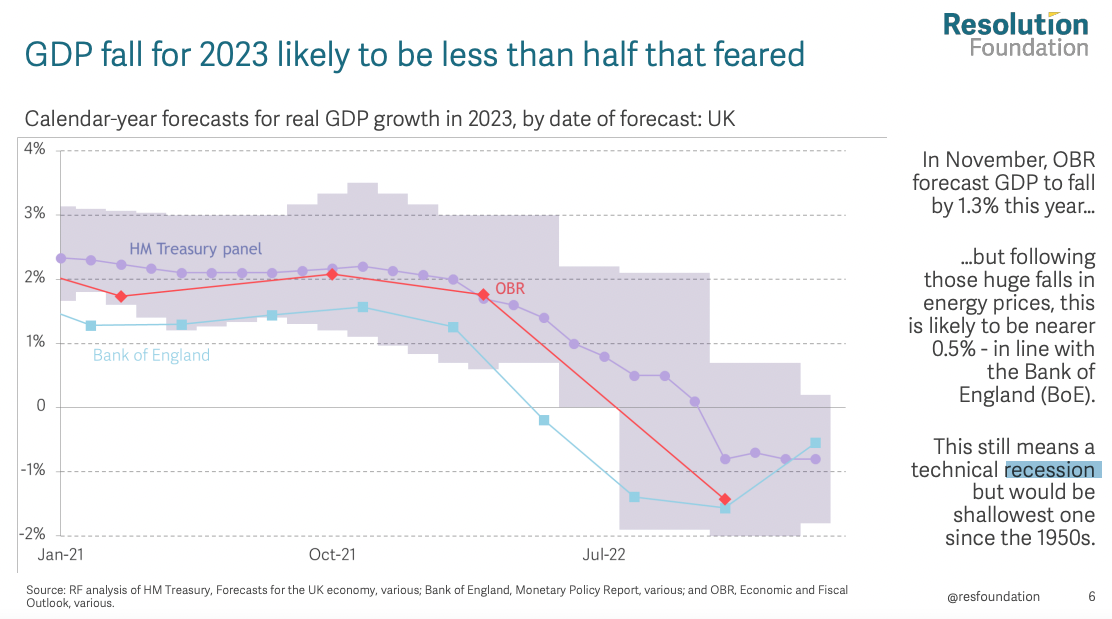

The Resolution Foundation predicts that we will still go into a “technical recession” (find out what that means here) but it is likely to be the shallowest one we have seen since the 1950s.

The GDP fall is likely to be less than half of what was feared, mainly because of those huge falls in energy prices. In November, the OBR predicted GDP would fall by 1.3 per cent this year. But now it is likely to be nearer the 0.5 per cent mark, in line with the Bank of England’s predictions.

Will our taxes go up in the Spring Statement?

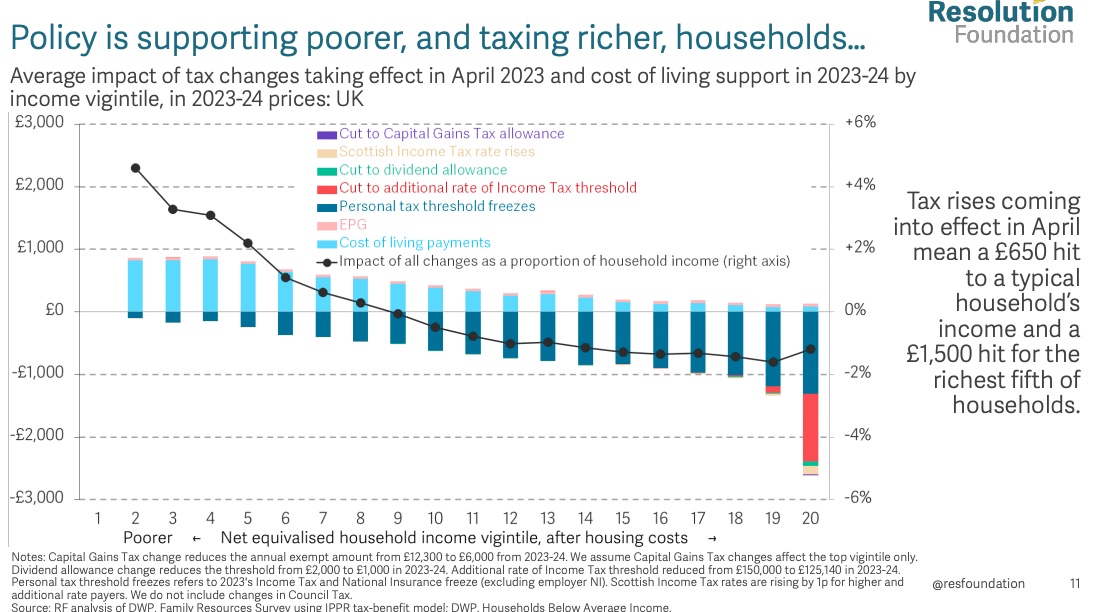

Brace yourself: the average amount paid in taxes is set to rise after the Spring Statement to help pay for the cost of living crisis and rising costs. Taxes aren’t going up exactly, but through a mechanism called fiscal drag people will end up paying a bit more. Here’s how it works.

The personal tax allowance is the amount you can earn before you pay tax, and tax rate thresholds are the point at which the percentage of your income you pay in tax goes up. Both are being frozen until 2028, meaning as people’s incomes rise through inflation, the government is able to collect more money from tax.

Want explainers like this straight to your inbox? Sign up to our newsletter here:

Advertising helps fund Big Issue’s mission to end poverty

Say you earn the average salary of £33,000. Your first £12,570 is tax free, and after that you are taxed at the 20 per cent tax rate. People earning over £50,000 pay 40 per cent tax, and those earning over £150,000 pay 45 per cent. As inflation rises and salaries increase accordingly, people will reach those thresholds faster and end up paying more in tax overall.

So tax payments are expected to go up by £650 a year for the average household from April, according to the Resolution Foundation, but lower income households are unlikely to end up worse off. It’s higher for the richest fifth of households, going up to around £1,500 but, of course, their high incomes should be enough to cushion the blow to their finances.

What is happening with the cost of living payments?

The government has already announced there will be cost of living payments for low-income households between Spring 2023 and 2024. It is unlikely to announce any more targeted payments after this point.

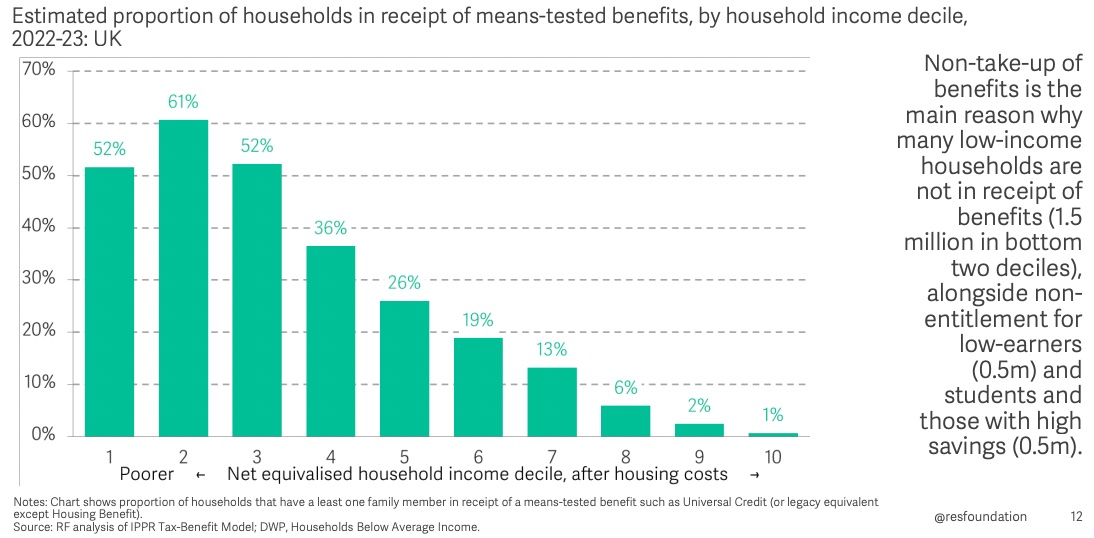

But as the Resolution Foundation points out, not all poorer households will get cost of living payments. This is mainly because there are 1.5 million people in the two lowest income groups who don’t get benefits, simply because they haven’t applied. There are also half a million low-earners who are not eligible for benefits, and most university students aren’t eligible either.

Are benefits going up in line with inflation?

The government promised to increase benefits in line with inflation from April – and they are increasing by 10.1 per cent. But campaigners warn it is “too little, too late” to help low-income families who cannot afford the basics needed to live.

Universal credit claimants will be £140 short of the money needed to afford the essentials each month even after benefits increase, according to analysis from the Trussell Trust and Joseph Rowntree Foundation (JRF).

Advertising helps fund Big Issue’s mission to end poverty

And research from the Institute for Fiscal Studies (IFS) showed benefits claimants will be 6 per cent worse off in real terms than they were in 2019. That’s because rises are based on inflation figures from months before the increase actually comes in.

Will the government scrap planned rises in fuel duty?

The Resolution Foundation has said the government is likely to scrap some (if not all) of the planned rises to fuel duty. If the duty cut was to be removed as originally planned, the RAC says current petrol prices would rise to 153.72p (up from 147.72p) and diesel to 173.19p (up from 167.19p) when factoring in VAT. The Resolution Foundation goes further and says the increases could add up to 12p/litre to prices.

Cancelling all planned rises would cost £5bn, according to the Resolution Foundation. That falls to £3bn if just the RPI rise is scrapped.

The Big Issue’s #BigFutures campaign is calling for investment in decent and affordable housing, ending the low wage economy, and millions of green jobs. The last 10 years of austerity and cuts to public services have failed to deliver better living standards for people in this country. Sign the open letter and demand a better future.

Advertising helps fund Big Issue’s mission to end poverty

Advertising helps fund Big Issue’s mission to end poverty