‘You live in fear’: Leasehold homeowners share horror stories of nasty hidden fees and service charges

The government had promised to get rid of the ‘feudal’ leasehold system. Instead, residents are stuck in a house of mirrors while reforms remain elusive

by:

29 May 2024

Housing secretary Michael Gove had previously promised to abolish leasehold. Image: Big Issue illustration/UK Government/Tim Hammond via Flickr

Share

Tough choice, isn’t it? Spend the rest of your life renting, or suck it up and buy whatever property you can afford. In big cities where only flats are within the reach of most, leasehold remains the main way to enter the housing casino.

It’s a feudal system which needs getting rid of. Those aren’t our words – it’s the opinion of the ruling Conservative government. But those manifesto promises have translated into rushed-through and watered-down reforms. In the meantime, residents suffer.

It’s left to individual residents to take on what amounts to a second job, spending evenings combing through spreadsheets to ensure they’re not ripped off.

Those who take the time discover all manner of abuses, hardwired into the system, and done within the rules. Managing agents skim – perfectly legally – thousands off the top of insurance policies. Residents pay insurance premiums for houses that burned down in another county. Companies thank residents for spotting mistaken charges totalling hundreds of pounds.

These are the stories we’ve discovered from speaking to four leaseholders from across the country – cautionary tales from the pre-collapse glory days for freeholders.

‘I bought leasehold against my best judgement’

Adam Bond was pleased to buy his three-bed maisonette in Exning, a small village in Suffolk near to where he grew up. There was a catch – although one he didn’t fully appreciate at the time.

Advertising helps fund Big Issue’s mission to end poverty

Advertisement

“The compromise was buying leasehold, which I swore I would never do, and I did against my best judgement,” he says. “But that said, at the time it was able to secure me a three bedroom property for money that I could actually afford to pay”.

When he picked up the keys in 2006, the service charges were nothing to really worry about, costing him £99 a year. Skip to 2025, and the bill is now £934 a year, with more than a third of that coming from buildings insurance. From 2024 to 2025, his bill jumped from £78 to £380.

The cost of insurance across the board has shot up recently. But when Bond started digging, he discovered something beyond this. His managing company, Flagship, insures all its leasehold and shared ownership properties under a single group policy, covering a total of £654m worth of property.

“Flagship are, in effect, having our block of leaseholders subsidising insurance for much higher risk properties, who’ve made enormous claims including some completely destroyed by fire,” says Bond

The fact Bond owns his flat as a leaseholder means he has no power to arrange his own insurance, or for everyone in his block to do so. He’s stuck, paying a premium for accidents happening – in some cases – in another county.

A list of claims made under the policy, uncovered by Bond, shows some of the biggest payouts in recent years, including fire damage claims of £102,000 and £88,217, as well as a £63,000 claim for subsidence.

Advertising helps fund Big Issue’s mission to end poverty

Flagship says a number of factors have increased insurance costs: fewer companies offering insurance, a higher cost of materials if properties need to be rebuilt, a higher cost of temporary accommodation while repairs are done, high inflation, and increased flooding and storms. A policy review document argues that a single policy is necessary to prevent dealing with separate insurers in the case of a claim, and to prevent any properties remaining uninsured.

Yet Bond feels the group policy, and the lack of choice it affords, is unfair.

“It would be bad enough if someone else in my block that I’m in made a claim and it pushed my costs up. But for a house to burn down in a different county and my bill to go up over five times?” he says.

Discovering this, and putting his case to Flagship, has not been simple. He has A4 files of correspondence, reams of digital records, and spends hours drafting and redrafting emails. He estimates it’s taken him weeks worth of hours to liaise, argue, complain and obtain documents.

“It’s incredibly frustrating. I feel like it’s a constant battle. With them constantly trying to put up the service charges. And us having to fight back against that, contest it,” he says.

Jonathan McManus, Flagship’s chief financial officer, said: “We have done and will continue to do everything we can to ensure value for money and keep costs as low as possible, while ensuring our leaseholders have appropriate cover and peace of mind”.

Advertising helps fund Big Issue’s mission to end poverty

‘You just live in fear of the next bill dropping’

Insurance is an issue for Stephen Squires, too. He lives in a two bedroom flat in Manchester city centre. Since buying the flat in 2013, his service charges have gone from £331 a quarter to £676 a quarter, in part due to cladding remediation work being needed as a result of the new Buildings Safety Act.

“We are really struggling alongside other bills and outgoings,” he says.

Squires discovered his managing agent makes thousands in commission from his building’s insurance policy. Image: Supplied

But it’s his insurance bill which particularly rankles. The total cost of his block’s insurance policy, covering 165 leaseholders, is £80,937 a year. You may expect all of this to go towards the cost of insuring the block. It does not. Homeground, the managing agent, takes a £5,351 commission. The insurance broker then takes £4,258, bringing the total commission paid to 11.8% of the money Squires and his fellow residents hand over.

This is currently perfectly legal, but often not something residents are told ahead of time. In a sample of 16 brokers carried out by the Financial Conduct Authority, residents ended up paying over £80m in commission. Firms aren’t allowed to recommend a policy purely based on the level of insurance, and must tell leaseholders if any commission has been paid. Housing secretary Michael Gove had promised to ban the practice.

In the meantime, it’s contributing to bills that keep growing. “The problem is we’ve got no control over it whatsoever,” says Squires. “As leaseholders we are completely at the behest of the freeholder and the managing agent.

“If the cost doubled next year, there’s nothing we can do about that. You just live in fear of the next bill dropping,” he adds.

Advertising helps fund Big Issue’s mission to end poverty

The high bills have made Squires and his neighbours band together to scrutinise exactly what they’re paying for. It takes hours – residents meetings, emails challenging costs and asking for explanations. Simple emails can often take a couple of hours. “You never get a full answer to a question, you get half an answer,” he says.

Squires spends hours going through spreadsheets and drafting emails. Image: Supplied

“It’s always on your mind, even when you’re not sat writing letters,” Squires says.

“It ruins the whole dream of home ownership.”

‘It’s an absolute world of pain’

For the most part, leasehold brings to mind high-rise flats and sprawling estates. But for Susannah Wise, leasehold looks like the upstairs flat in a Victorian terrace in north London.

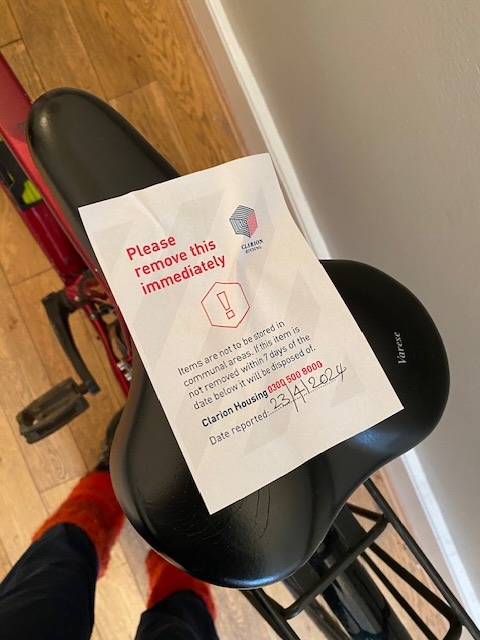

After she speaks to the Big Issue, she sends a photo from her communal hallway. Workers acting on behalf of Clarion – her freeholder – have let themselves in, and put a “notice to remove” sticker on her bike seat. Completely within the rules, you see – Wise’s bike is a trip hazard, and rules need to be enforced consistently across all Clarion properties.

‘It’s an absolute world of pain’, says leaseholder Susannah Wise. Image: Supplied

Until Wise, an actor by day, turned amateur sleuth, she was paying over the odds. At the time, her service charges were £790 a year, with management fees making up £260 of this. Then she spotted a clause in her lease, saying management fees should account for no more than 10% of service charges – or £79 of that bill.

Advertising helps fund Big Issue’s mission to end poverty

“I’ve had time to follow all these things up. It’s like a full time job, it’s been taking up so much of my time,“ she says.

It took an escalation to the Housing Ombudsman to set things right. In total, she’s received £1,735 in refunded management fees, £46.38 in admin fees, and £700 in compensation

“To my mind that wasn’t acceptable. You can’t just say ‘oh we suddenly realised’ now you’ve been called out. I would never, ever buy another Clarion leasehold property. I probably won’t buy another housing association leasehold flat again. Because it’s an absolute world of pain.

“It’s very, very stressful, it affects you on an energetic level, and on a mental health level, and on a physical health level.”

The notice left on Wise’s bike seat. Image: Supplied

A spokesperson for Clarion said: “We’re sorry for the inconvenience caused to Ms Wise and that our service fell short of what we expect for our customers.

“The service charge error has now been corrected and we can confirm that the current management fee is within the terms provided in the lease agreement.

Advertising helps fund Big Issue’s mission to end poverty

“In addition, we have reimbursed Ms Wise all overcharged fees as well as offering a compensation in recognition of the failure in our service.”

‘We welcome scrutiny from our customers’

Could a cavalier attitude to overcharging until you’re caught be part of the business model? Judge for yourself with this statement from the housing association Hyde: “We welcome scrutiny from our customers and will set things right where we’ve made mistakes.”

Hyde sent us this statement after we asked about the case of Simona Pau. Thanks to overcharged service charges, including being asked to pay for services she does not receive, Pau received a total of £682 in refunds between 2019 and 2022, as well as £100 compensation.

Her 2023/24 estimated service charges went down from £2038.20 to £1274.76 when she disputed services they don’t have – such as a controlled door. Again, Pau only got the money back after devoting evenings and entire Sundays to digging, prompted by rapid increases in her annual bills. “It really is a second job,” she said. Now, she’s paying just 70% of the service charges Hyde are asking for until disputes are resolved.

“If people don’t pay attention, they just pay. This is what we were doing initially before noticing the charges were increasing,” she says.

“It’s a stressful thing to do, to constantly be on top of everything,” adds Pau”

Advertising helps fund Big Issue’s mission to end poverty

“I know that my time is precious but I don’t want them to get away with it.”

Hyde, which deals with over 1million invoices each year, apologised for the errors and said its service charge estimates are getting more accurate each year.

“We’re very conscious of the cost-of-living crisis and the pressure that’s being put on our customers. We’re doing everything we can to help by negotiating better prices with our suppliers and by being more efficient in the way we do things. We do not make any profit from service charges and only recover costs that we have incurred for providing services to customers,” a spokesperson said.

“Unfortunately, the cost of providing some of the services to keep our homes and buildings decent and safe has increased this year, particularly around energy, building safety and buildings insurance.”

Advertising helps fund Big Issue’s mission to end poverty